In a new blog post, Magnus Söderberg dives into the Web3 games' reality check following the BGA's 2025 State of the Industry report, in which 64% of builders now see regulation as an engine of growth rather than a threat. He shows how years of fraud, Ponzi-like token models and short-lived projects have pushed the sector towards trust, compliance, stablecoins and product-driven design as the new basic standard for sustainable growth.

Magnus Söderberg is a Swedish gaming entrepreneur and Founder & CEO of Triolith Games AB. He has spent more than 15 years building and scaling game studios, including Triolith Entertainment, Gold Town Games, and Vorto Gaming. A long-time Web3 and P2E researcher with 15,000+ hours in Entropia Universe, he focuses on fair game economies, player protection, and compliance-first infrastructure for the next generation of Web3 games.

The 2025 Blockchain Game Alliance (BGA) State of the Industry Report marks a definitive break with the last cycle. Web3 gaming is moving from speculative experiments to an era defined by regulation, trust, and product discipline. The most critical shift? Nearly two-thirds of industry professionals now say policy and regulation will help the sector grow, not hold it back.

This isn’t a mood swing. It’s a structural reset.

The BGA report describes a sector “moving beyond its speculative origins toward a more operationally disciplined, product-led future.”

The euphoric funding of 2021–2022 has fallen sharply. Many heavily marketed titles never reached sustainable player numbers. Others shut down after short lifespans, stranding users and evaporating the promise of “own your assets forever.”

Yet, the report is not apocalyptic. It shows a community that is bruised but still building. Activity remains high, but it’s less visible, fragmented across platforms, chains, and regions. The difference is that survival now depends on proven product-market fit, not token velocity.

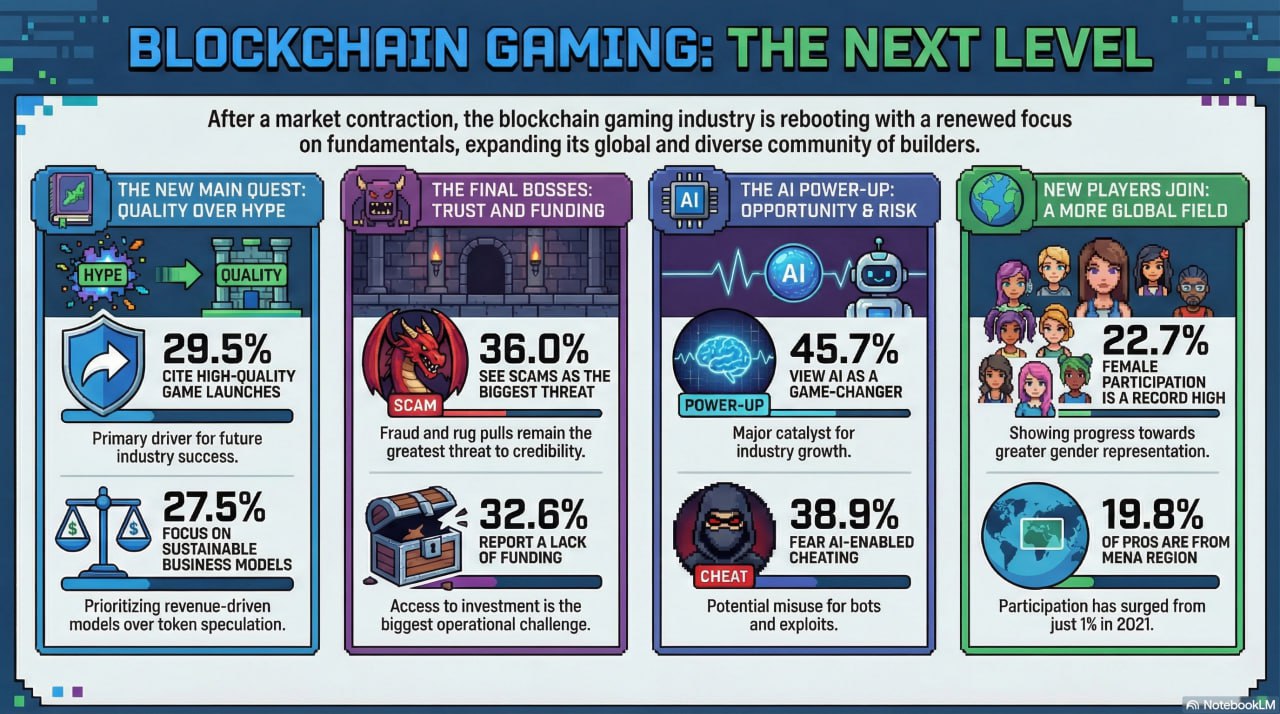

In 2021, “regulatory uncertainty” was one of the top three challenges cited by respondents. Today, 64.4% expect policy and regulation to have a positive impact on the industry.

That shift is profound and speaks to the market’s fatigue. It suggests that:

The report links this newfound optimism to concrete developments: MiCA in Europe, clearer stablecoin frameworks in the US and beyond, and more structured approaches emerging across Asia, MENA, and Latin America.

In practice, this means that “ship now, ask lawyers later” is no longer a viable strategy for studios that want to outlast a single market cycle.

When respondents were asked about the greatest threat to blockchain gaming’s credibility, the answer was blunt: scams, fraud, and rug pulls. 36.0% picked this as the top risk, ahead of regulation, volatility, or even game quality.

A further 12.6% pointed to Ponzi-style economic models, and 20.4% highlighted poor-quality games. Together, they paint a picture of an industry whose main wounds are self-inflicted: unstable economies, opaque token sales, and projects that over-financialized the experience while under-delivering on fun.

The takeaway is clear. The problem isn’t the underlying technology; it’s governance, incentives, and basic accountability. The sector doesn’t need fewer experiments; it needs fewer experiments where players and investors carry all the downside risk.

At a company level, 32.6% of respondents say lack of funding or investment is their biggest operational challenge.

Zoom out, and the narrative changes. The report interprets the funding pullback as a healthy market correction rather than a death sentence. Easy capital has disappeared, but what remains is more demanding:

The same survey shows what respondents believe will actually drive the next wave of growth: 29.5% point to high-quality game launches, and 27.5% to sustainable, revenue-driven business models.

In other words, the market is quietly shifting from “What’s your Fully Diluted Valuation (FDV)?” to “Can this game retain players and pay for itself?”

One of the more understated but essential findings of the report is the growing role of stablecoins and payment infrastructure.

Stablecoins are framed as a practical backbone for real-world commerce in games—offering faster settlement, reduced cross-border friction, more predictable pricing for players, and easier integration into existing payment APIs.

This isn't just about payments; it's about removing volatility from the core loop. Players don't want their tournament winnings to swing 30% in a week. Studios can't pay server bills with hype. Stablecoins provide the boring, reliable rails that allow the fun part of the economy to flourish on top.

Alongside this, interviewees highlight the importance of invisible infrastructure: faster, more reliable wallets, account abstraction, and multi-platform distribution.

None of this is glamorous, but this foundational layer will decide whether a successful game can scale beyond a niche crypto audience.

For studios still in the game, the BGA report functions almost like a set of non-negotiable design constraints:

The 2025 BGA report doesn’t declare victory for blockchain gaming. It documents a sector in the middle of a painful but necessary evolution.

The easy money has gone. The tolerance for scams and sloppy design is shrinking. The regulatory no-man’s-land is slowly being replaced by real frameworks, and for most builders, this is a relief rather than a source of anger.

If the last cycle was about proving that on-chain games could exist at all, the next one will be about proving that they deserve to.

What is the main message of the BGA 2025 State of the Industry Report? The report shows blockchain gaming moving from speculative, token-driven experiments toward a more disciplined, product-led phase. Trust, regulation, and sustainable revenue models now matter more than hype, even as funding remains tight.

Why are 64.4% of respondents now positive on regulation? After years of operating in legal grey areas, studios, investors, and infrastructure teams increasingly see clear policy as a stabilizing force. It reduces uncertainty, encourages institutional participation, and gives long-term projects a clearer path to scale.

What does the report identify as the biggest threat to Web3 gaming? The top threat is not technology, but trust: 36.0% of respondents name scams, fraud, and rug pulls as the main credibility risk, followed by Ponzi-style economies and low-quality games. Together, these self-inflicted issues remain the biggest barrier to mainstream adoption.

How should studios react to the funding and user acquisition challenges? With 32.6% reporting lack of funding as their main challenge, the report suggests a pivot toward leaner teams, faster validation, and revenue-driven models. Teams that can attract and retain players without relying on token incentives alone are the most likely to survive the shakeout.

Where do stablecoins fit into the future of blockchain games? Stablecoins are presented as a core payments and settlement layer: ideal for cross-border payouts, prize pools, marketplace transactions, and integrating with mainstream payment APIs. They support more predictable player experiences than volatile native tokens alone.