Norwegian fintech is now showing positive signs in terms of revenue and profitability. Regulatory conditions and technology developments represent challenges, but there are also new opportunities, including in artificial intelligence, blockchain and tokenization.

This is evidenced by a report on Norwegian fintech in 2024, which Per Fredrik Forsberg Johnsen (right) of Menon Economics on Wednesday presented in a breakfast seminar hosted and moderated by the Finance Federation at Lars Øystein Eriksen (left).

The Finnish Finance Federation has commissioned the report, which has been prepared for many years, and this year delivered by Menon Economics.

“We do this to map the economic development and role of fintech companies in Norway. At the same time, it is important to shed light on the strategic opportunity space for companies in relation to regulatory changes and technological developments, said Lars Øystein Eriksen at the opening of the breakfast seminar.

In his presentation of the report, Forsberg Johnsen emphasized that fintech is a highly technology-driven industry that delivers into a distinct value chain, namely finance. It also makes fintech a relatively large single industry within the Norwegian startup system.

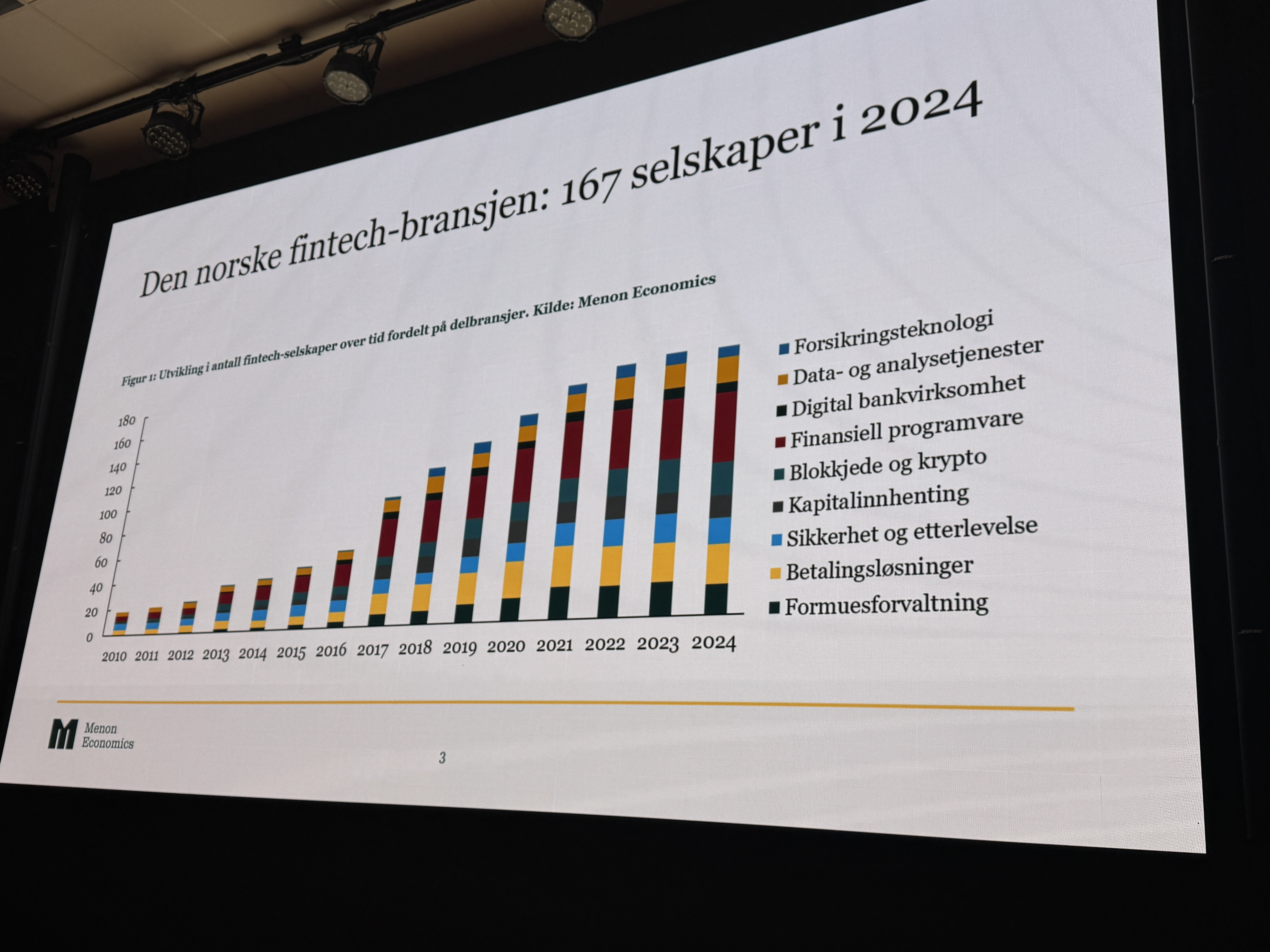

The report defines 167 companies divided into nine sub-industries. Forsberg Johnsen described that the development has taken place in three phases: first with moderate growth until 2016, then a very good influx of new fintech companies until 2022, while since 2022 there has been a flattening. Forsberg Johnsen added that this could be a sign of concern, but the other figures he presented reduced this concern.

Despite the fact that there has not been a large influx of new companies, there has been persistently high revenue growth in the industry. If you include blockchain and crypto as well as Sbanken and Bank Norwegian, the turnover is almost NOK 30 billion. If you exclude them, the figure is about half. The largest sub-industries in terms of revenue are digital banking, payment solutions, wealth management, and security and compliance.

The industry shows a profit for the first time since 2020, if you include Sbanken and Bank Norwegian. The main driver here is digital banking with an industry-level profit of NOK 600 million, but almost all sub-industries show increased profitability. Forsberg Johnsen saw this as a sign that more fintech businesses are maturing, in that deficits are being reduced or replaced with surpluses. Productivity has been rising for the past couple of years, and is lower than established finance, but at the same time higher than start-up business in general.

In terms of employment, there has been a steady increase. In 2024, the growth in the number of employees was 14 percent, which is the strongest growth in four years. Here, financial software and payment solutions predominate. According to the report, the value added to society — that is, the industry's contribution to GDP — amounts to NOK 5 billion. Here digital banks, security and compliance as well as financial software dominate.

According to the report, the industry is characterized by an interplay between regulations, capital and technology. The regulations often create a competitive disadvantage, where implementation of EEA rules is perceived as demanding. When it comes to access to capital, it is consistently considered a challenge, which is also related to the Norwegian tax system. On the technology side, artificial intelligence is changing the industry, creating both opportunities and challenges. Blockchain and decentralized finance will also affect development, according to Forsberg Johnsen — regardless of what opinions one may have.

In addition to regulation and embedded finance, blockchain, tokenization and artificial intelligence were highlighted as key areas for the way forward.

This is how these four areas of possibility were described: